The numbers numb the mind; stun our sense of proportion: the biggest public issue in India’s stock market history, which will raise Rs 1 trillion later this year! And tens of millions of investors who may buy these shares. The part disinvestment of Life Insurance Corporation (LIC) will affect millions of policyholders and 1.2 million agents. The sale may be an investment game-changer. The financial rhythm of urban India will fluctuate as people debate its pros and cons over the next few months.

For, LIC is a brand that unites India. It is a name that resonates with, and reassures, most Indians, both in urban and rural areas. Prime Minister Narendra Modi, Finance Minister Nirmala Sitharaman, Amitabh Bachchan, the Bollywood celebrity, you, and I have invested in LIC policies. Each year, around this time, before end-March, taxpayers scramble around to buy them to save taxes. Almost like clockwork, the LIC agents come knocking at their doors.

Excitement reigned within the investor community after Sitharaman unveiled the changes to the LIC Act in her third Budget. If passed by Parliament, they will pave the way for the listing of insurance giant on the bourses. You and I, apart from being the buyers of its policies, may be proud owners too. Still, some of us, along with anxious agents, are plagued with worries. As the government prepares to offload possibly a tenth of its 100 per cent holding in LIC, we are a bit unsure.

Finance minister Nirmala Sitharaman on her way to present the Union Budget 2021-22.

However, as part of her budget, the finance minister tried to balance the interests of different stakeholders, including investors, policyholders, agents, and foreign competitors. For example, the biggest fear among enthusiastic small investors is that they will be priced out of the proposed Initial Public Offering (IPO). This stems from the size of LIC’s share capital, which stood at Rs 1 billion as on March 31, 2020. At a face value of Rs 10 per share, this translated into 100 million shares.

Although the official valuation of LIC as a company isn’t available, RBSA Advisors, an independent valuation firm, pegged it last year at between Rs 9.9 trillion (12 zeroes) and Rs 11.5 trillion. Hence, the price per share comes to Rs 99,000-115,000. Obviously, when the government sells a part of its holdings, a retail investor may find it tough to buy five shares, and impossible to think of 10. To assuage such concerns, the government may hike the share capital and, hence, the number of shares it owns.

If the first figure goes up from the existing Rs 1 billion to Rs 3 billion, there will be 300 million shares of Rs 10 each. The overall valuation of the company will remain the same, but the per-share price drops by a third to Rs 33,000-Rs 38,333. Therefore, you can buy 10, or more, shares. “The government may ensure that the price per share during the IPO is in three digits (a few hundred rupees) to maximise participation by retail investors,” says Vankatraghavan S. of Equirus Capital.

For extra safety, the changes to the LIC Act allow the insurer to boost the share capital to as high as Rs 250 billion, or 25 billion shares. This will make the share enticing, as its price will tumble down to around Rs 400 each. However, it implies that the government will need to pump in the additional Rs 249 billion to raise the equity. It may, therefore, settle at a mid-point solution—the share price remains below Rs 1,000, and the finance ministry invests Rs 100 billion to Rs 125 billion.

While this may energise the investors, it irks the experts. A former LIC chairman agrees that the price will remain in the Rs 400-1,000 band, it will undervalue the company. “We know that it (LIC) is capable of much more,” he says. What he implies obliquely is that the value of a share of LIC, given the company’s size (first-year premium of Rs 1.78 trillion in 2019-20) and market share (almost 76 per cent in terms of new policies in 2019-20), is higher than the government’s numbers.

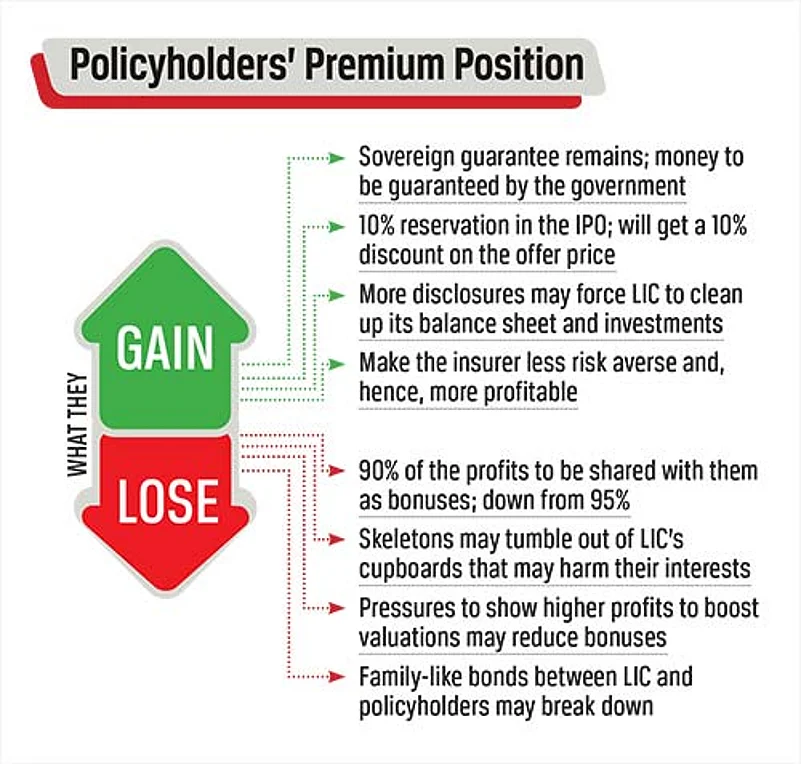

If the investors want a lower share price, policyholders want higher bonuses that LIC magnanimously doles out every year. In the first six months of 2020-21, policyholders received Rs 510 billion as bonuses. At present, LIC shares 95 per cent of its annual profits with policyholders and pays the remaining to the government. The changes in the Act will lower this to 90 per cent. This raises the concern that shareholders (government plus new ones through the IPO) will gain as they rake in 10 per cent.

“This may reduce interest in LIC policies. The profits shared with the policyholders can decrease if the government divests more shares later,” says Devi Shankar Shukla, president, Life Insurance Agents’ Federation of India. SEBI rules require that a company with a market capitalisation of more than Rs 40 billion has to dilute at least 10 per cent during the IPO, and another 15 per cent within three years. The changes in the LIC Act provide for a further dilution of government’s stake to 75 per cent.

However, in a bid to get policyholders on its side and encourage them to continue with LIC, the government offers two crucial sops. The first relates to the sovereign guarantee—the money invested by the buyers of policies is guaranteed by the government. There was a dread that this may go, thanks to the persistent demand by the foreign insurers, which compete with LIC, for a level-playing field. The sovereign guarantee hugely tips the scales in LIC’s favour.

“Neither the Budget speech nor the Finance Bill (which lists out the changes to the LIC Act) contemplate amendments to the sovereign guarantee clause,” says Aravind Venugopal, partner, Khaitan and Company, a law firm. In her post-Budget press conference, Sitharaman said that the guarantee will continue, much to the relief of the policyholders and LIC agents. Shukla adds, “The policyholders bought into government-backed schemes, and this is why they trusted LIC.”

At the same time, the government has stated its intention to reserve 10 per cent of the IPO for LIC’s existing policyholders. In addition, they will get a 10 per cent discount on the offer price, as and when the issue comes out. “On the face of it, the discount means that they will gain 11 per cent compared to other investors. SEBI, which allows reservation for only retail investors and employees, may grant an exemption in this case for policyholders,” predicts Venkatraghavan.

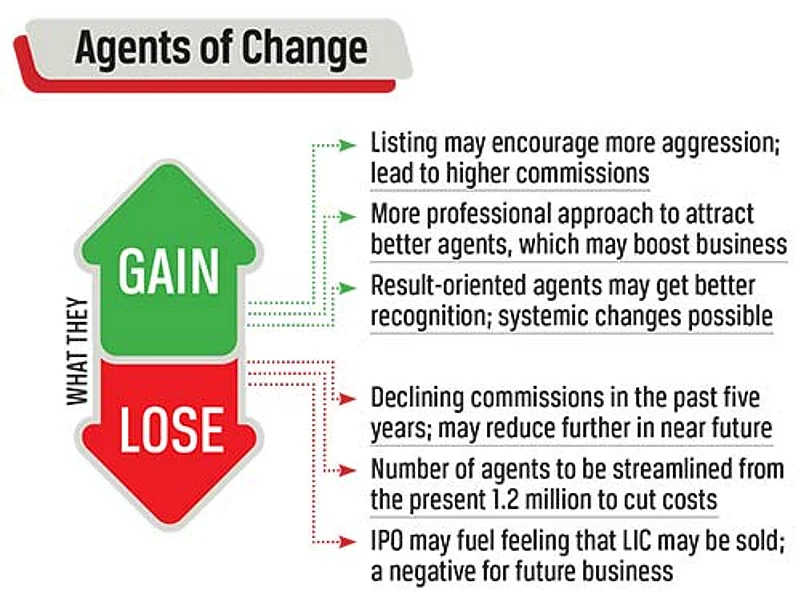

Both these moves related to guarantee and reservation cheered the 1.2 million LIC agents, who feel they are part of an extended family. Many owe their existence and prosperity to the insurer. “It is not just an insurance company. It is actually a big brother in our family. While I took care of my clients, LIC took good care of me,” contends Ashok Kumar, 53, a Chennai-based LIC agent who earns Rs 2 million a month, and graduated from a bicycle to a chauffeur-driven SUV in less than a decade.

In 2011, Kumar became the third family member to become an agent. First, his mother passed the agent’s entrance exam when she was 55 and retired after six years. She was followed by his wife, Krishna Prema, who later opted to listen to religious discourses. A Delhi-based LIC agent, P.K. Soni, says that LIC enabled him to build a house, marry off his daughter, and take care of his post-retirement nest. “Being an agent assures regular income and provides opportunities to grow,” he adds.

Despite their great esteem for the insurer, Soni and Kumar are cagey about the IPO. They, like others, feel that the agents’ commissions, which totalled massive Rs 201 billion in 2019-20, may be slashed, as company focuses on profits due to its listing. There will be pressure from new shareholders to enhance stock valuation. “Although they are the best among competition, the commissions have come down over the past five years, and may reduce further,” says Soni.

Shamsher Singh, a Punjab-based LIC agent, adds, “We face the heat in rural areas due to negative sentiments on the three farm laws and the growing feeling that the government will sell LIC.” This is despite the fact that changes to the LIC Act categorically state that the government will never dilute its stake below 51 per cent. As of now, the company will not be privatised or sold. But, as public perception goes, the near future looks uncertain, given this regime’s aim to get out of businesses.

An annexure attached to the Budget speech states that state-owned units will henceforth be divided into strategic, which includes crucial areas such as insurance, banking, atomic energy, space, defence and minerals, and non-strategic ones. The first will witness “bare minimum presence” of the public sector. Apart from this minimal number, the rest will be privatised, merged with other state-owned units, or closed. In the non-strategic areas, everything will be sold or closed.

So, the hammer can fall on LIC despite the government’s commitment not to sell it. There are indications from the manner in which the foreign direct investment (FDI) limit in the insurance sector was hiked from 49 to 74 per cent. This may spur the entry of large global players, who want greater control over their Indian operations. Although they will be piqued by the continuation of sovereign guarantee to LIC, they will be in a position to nudge policy-makers to withdraw it later.

But foreign competitors will be happy on two counts. The first is reduction in the percentage of the LIC’s profits that can be paid as bonuses to policyholders. This brings the state-owned insurer at par with the private firms. The second is the change in the corporate status of LIC, which will be governed by the Companies Act and SEBI laws. These will lead to transparency and disclosures. Thus, one will know as much about the state insurer as we do about the others.

This leaves us with the last section that has to be perked up before the IPO—around 1,00,000 LIC employees. They have opposed divestment. However, as an insider reveals, their number may dwindle down to 50,000 by 2025, as existing people will retire and fresh recruitment, as in the recent past, may remain slow. Another insider says that the best way for the government to get the employees on its side is to reserve a portion of the IPO for them, as it may do for policyholders.

Clearly, the government wishes to get various stakeholders, as well as competitors, on board for the gigantic LIC IPO. If successful, it can become the springboard for the launch of other huge public issues. In her Budget speech, the finance minister said that a state-owned general insurance firm, as opposed to a life insurance one, and two public sector banks, apart from IDBI Bank, would also be put on the auction block. These, too, are likely to happen in 2021.

Will the privatisation party turn into a wild one this year, with huge cheers from investors?

***

Blown Cover

- LIC IPO in 2021; amendments included in Finance Bill

- IPOs of state-owned general insurance firm and two banks

- Minimal presence in insurance; but stake in LIC to be 51% and above

- FDI limit in insurance hiked from 49% to 74%; woo private players

- ULIPs above certain annual premium to be taxed

By Yagnesh Kansara and Jyotika Sood with inputs from G.C. Shekhar, Vishav, Nirmala Konjengbam, and Himali Patel