Most people apply for a credit card because someone recommended it, or because the bank offered it pre-approved. A few months in, they realise the rewards are accumulating in categories they barely spend in, and the annual fee just landed with no easy waiver path. Kotak Bank's credit card portfolio is wide enough that the right card almost certainly exists; the gap is usually in how that decision gets made.

Kotak Mahindra Bank offers cards across categories spanning cashback, rewards, co-branded fuel benefits, entry-level digital access, and Signature-tier travel privileges. But what suits your needs? Let’s find out.

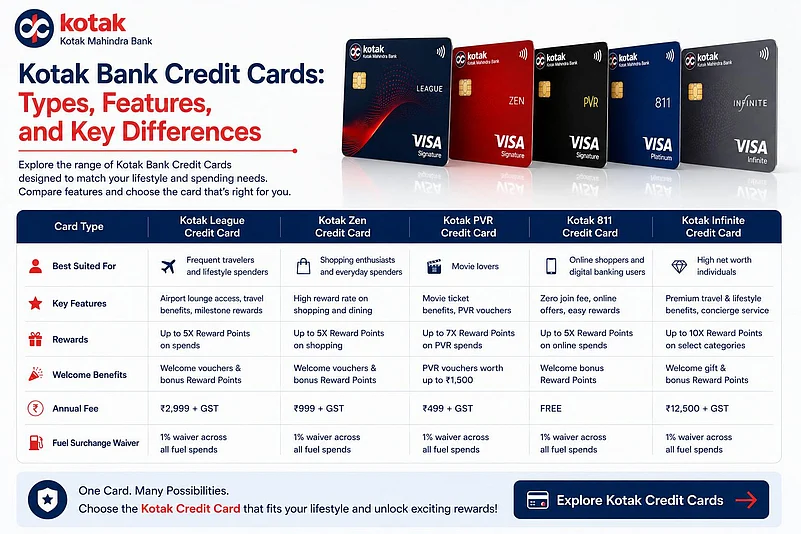

Types of Kotak Bank Credit Cards

Kotak Bank credit card portfolio broadly splits into several categories; each is designed around a different spending priority.

Rewards and Lifestyle: Cards designed around points on eligible spends with lifestyle-led privileges

Cashback: Straightforward statement-value cards with caps and waiver rules shown on Fees & Charges pages

Co-branded Travel: Airline-linked cards with partner-specific benefits and programme features

Fuel: IndianOil-linked benefits and programme integration as described on the product page

Entry-level: Digital-friendly access, including the Kotak 811 ecosystem

Premium: Elevated reward constructs and privileges on select variants

Key Kotak Bank Credit Cards and Their Features

The profiles below draw from information published on Kotak Mahindra Bank's website.

The Kotak 811 Credit Card is positioned more towards digital-first users and simpler onboarding. It fits the kind of customer who already prefers app-based banking and controlled spending instead of premium lifestyle benefits.

The Cashback Plus Credit Card, as the name suggests, focuses more on cashback-oriented spending categories. These cards usually attract users who don’t want the extra work of monitoring reward catalogues and conversion values constantly.

Travel-focused users may look at cards like the Indigo XL Credit Card, especially if flight bookings happen frequently enough to justify airline-linked benefits.

At the premium end, the Zen Signature Credit Card includes lifestyle and travel-oriented features like lounge access and reward-linked spends. Cards in this category tend to work better for higher monthly spending levels because the annual fee starts making sense only when the benefits are actively used.

Fuel-focused users usually look towards the IndianOil Credit Card because regular fuel spending can make surcharge waivers and fuel-linked rewards more noticeable over time.

And if you are looking for a card with lifestyle and rewards benefits, the Kotak League Platinum Credit Card is a good option for steady monthly spending.

Factors to Consider When Choosing a Kotak Credit Card

Spending pattern is the most important starting point.

A card with strong online rewards does very little for someone whose primary spending is offline, such as grocery or fuel.

Annual fee waiver thresholds matter almost as much as the fee itself; a ₹1,000 annual fee waived on ₹1 lakh spend costs nothing for a consistent high spender.

Reward redemption mechanics are worth reading carefully. Some Kotak cards redeem points at a fixed value; others have minimum redemption thresholds.

Complimentary benefits like lounge access or PVR tickets only deliver value if they align with actual usage. A cardholder who does not fly will not benefit from airport lounge access regardless of how many visits are included.

How to Apply for a Kotak Bank Credit Card

The online application process on Kotak Mahindra Bank's official website typically involves four steps.

Applicants select the card that suits their profile,

They fill in personal details, including PAN and income information,

Next, submit documents for verification, and

Finally, await the decision.

Salaried applicants with a clean CIBIL profile often receive decisions quickly.

Existing Kotak Bank savings account holders may qualify for pre-approved offers accessible through the bank's net banking portal or mobile app, which can reduce documentation requirements and processing time.

Conclusion

Kotak Mahindra Bank's credit card portfolio covers a genuinely wide range of user profiles — from someone opening their first credit account to a frequent international traveller seeking premium benefits. The decision is not difficult once spending behaviour is mapped honestly against the available options. Checking credit card eligibility before applying, understanding the fee waiver conditions, and reading the reward exclusions all contribute to a more useful long-term outcome. Interested users can explore current card details and apply through Kotak Mahindra Bank's official website.

Frequently Asked Questions

1. Is there a lifetime-free Kotak credit card?

Yes. The Kotak UPI RuPay Credit Card carries no joining or annual fee and is positioned as a lifetime-free card. It operates as a virtual card with UPI integration.

2. What is the interest rate on Kotak credit cards?

Please note that interest charges apply if the outstanding balance is not paid in full by the due date. Cardholders can refer to Kotak Bank’s website to check applicable terms and conditions for the latest interest rates and charges.

3. Can the annual fee be waived?

Several Kotak credit cards offer annual fee waivers on meeting a specified annual spend threshold. The 811 Credit Card waives its ₹500 annual fee on ₹50,000 spend. Conditions vary by card and should be confirmed on the Kotak website before applying.

4. Does applying for a Kotak credit card affect the CIBIL score?

A credit card application triggers a hard inquiry on the applicant's credit report, which can marginally reduce the CIBIL score. Applying selectively for cards where eligibility is likely minimises this impact.

Disclaimer: This is a sponsored article. All possible measures have been taken to ensure accuracy, reliability, timeliness and authenticity of the information; however Outlookindia.com does not take any liability for the same. Using of any information provided in the article is solely at the viewers’ discretion.