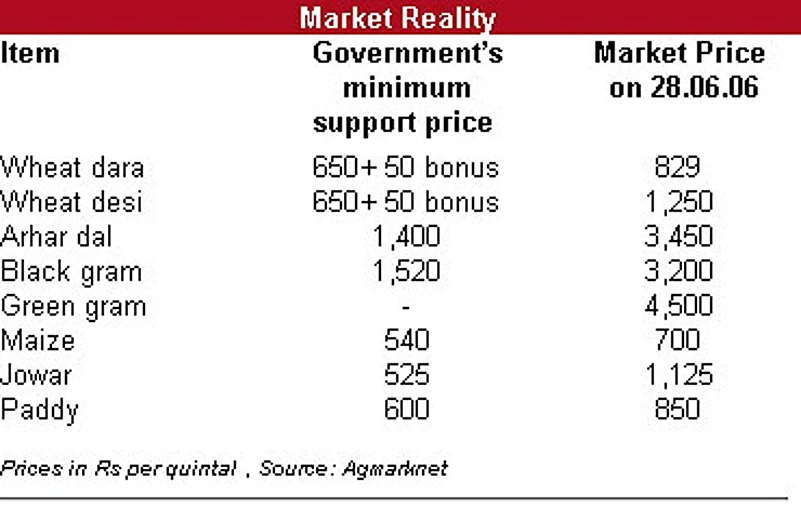

The most important reason was the very low opening stocks in almost all commodities which created a scarcity effect coupled with lower produce. In wheat, pulses, mustard and red chillies, opening prices this year have been higher than the peak prices of last year. This effectively killed harvest pressure, that is the depressing effect of the new crop arrival on prices. In wheat, private traders had less than three lakh tonnes as opening stock, compared to 10-15 mt a year ago, against a monthly demand of 5 mt. Even government stocks were at a five-year low of 6 mt. So all the current procurement went to meet current demand with little left for inventories. Now prices could go down only after the supply chain is replenished or when the traders feel assured about their supplies.

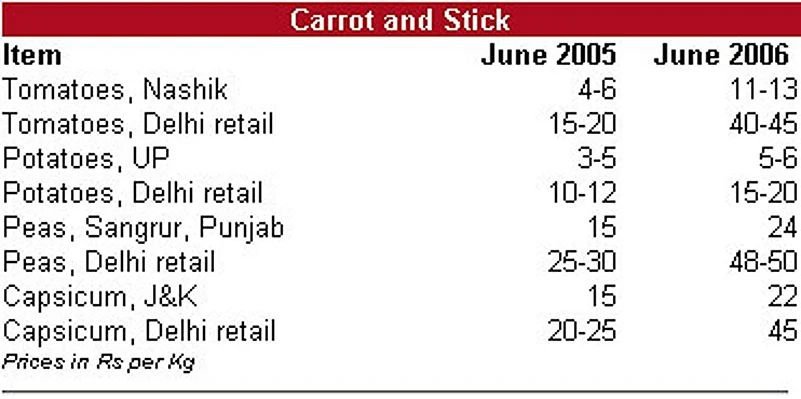

Which is what will happen to most vegetables like tomatoes. At Rs 45 a kg, or double of what it was even 15 days ago, the price of tomatoes has been affected by poor supplies due to a smaller early crop in Nashik, Maharashtra. The crop from Punjab and Haryana had anyway got over by early June. But when the crop from Solan in Himachal Pradesh comes in ten days and the next crop from Nashik in a month, prices will automatically come down.

Many primary commodities and vegetables have seen a poor crop this year, mostly due to lack of sufficient price or other incentives for farmers and erratic weather. Says Jaswinder Singh Bhondli of Samrala, Punjab, who grows vegetables on 28 acres: "April and May were hotter than usual and the problem was aggravated by shortage of electricity. High temperatures hit the crop and about 40-50 per cent of the crop was lost. I have suffered financial losses upto 20 per cent, while smaller farmers have lost more." In Nashik, last year's glut that caused a few farmer suicides has led to lower cropping. Then late rains, excessive heat and a pest virus ruined the early crop. According to the Maharashtra State Agriculture Marketing Board, over one lakh quintals of tomatoes came to the apmcs last June. This year, arrivals are down to half. In UP, potato farmers are celebrating higher prices—retail rates have gone up to Rs 8-10. "This year we got an opportunity to sell outside UP because of poor crop in Punjab," says Brijendra Sonkar, president of the Vegetable and Fruit Merchant Association.

Even the wheat crop is now expected to be less than 71 mt compared to a buoyant government estimate of 73 mt. The same over-optimism has affected the crop estimate for pulses which, like many other dryland crops, has been traditionally neglected. According to J.P. Thakur, president of the Azadpur market committee, the main wholesale vegetable market in Delhi, prices will stay high for a couple of more weeks till the supplying states recover.

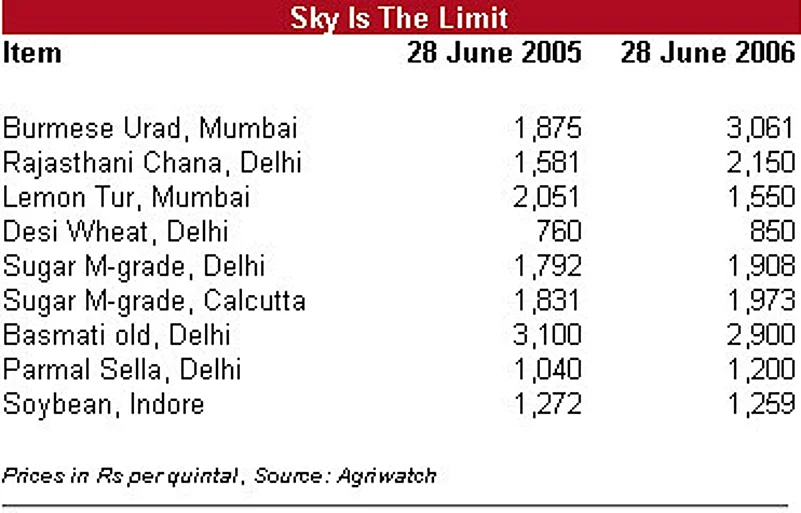

The second reason for the price rise logically follows from the short supply situation: speculative trading and hoarding. Praveen Khandelwal, secretary general of the Confederation of All India Traders (CAIT), says that low production coupled with high transportation costs due to the fuel price hike is the main reason for soaring prices. But he ignores the forward trading element in grains and pulses price rise. Explains Ramesh Chand, deputy director, NCAP, Pusa: "The price rise has to be seen from a broader perspectives of two new government policies, namely trading in commodity futures, and private buying from farmers at mandis. These big companies have the capacity to bear sufficient stocks and also enjoy considerable arbitrage opportunities." And with no stock limits, says Agriwatch, it is easy for these companies to show their muscle. To counter this, FCI officials had apparently sought government permission to intervene in the futures markets, which was not granted. But the government is now thinking of getting into futures trading in the next season.

Commodity futures trading, now allowed in all agri commodities including some perishable ones, has been a big success. Turnover has increased over four times from Rs 5,11,000 cr in 2004-05 to Rs 21,00,000 cr in 2005-06. But the situation was compounded by many operators on NCDEX and MCX, the two commodity exchanges, who manipulated their open interest positions to jack up prices. Ashok Singh Solanki, secretary, mandi samiti, UP, believes that the 'vayda bazaar (future trading)' has given rise to hoarding and inflation. The Forward Markets Commission has now cracked down on these operators, slapping fines. NCDEX too has raised margins on wheat by 10 per cent. But the damage is done, mostly to the FCI procurement effort. Compared to 13-14 mt every year, the government could get only 9 mt this time. Dr P.S. Rangi, marketing manager at the Punjab State Farmers Commission, estimates that private traders bought 13 per cent of the wheat against 2-3 per cent earlier.

In early April, trading on wheat futures for July and August touched a record high of Rs 950-1,016 per quintal, leading to massive hoarding. The anticipation of futures prices of Rs 1,200 in October-November fuelled big purchases by traders, commission agents, even rice millers. T.C. Gupta, FCI's senior regional manager who supervised wheat procurement in both Punjab and Haryana, says: "There was large-scale hoarding by big farmers. Around 15 lakh tonnes were withheld in Haryana. I've seen wheat stored on the premises of rice mills at Karnal and Khanna." At Khanna, Asia's largest grain market, 90 per cent went to private buyers.

The entry of large corporate houses also spurred the hoarding frenzy. The food processing sector growing at 20 per cent a year with giants like Reliance Agro, Godrej Foods, Sunil Mittal's Field Fresh (with Rothschild), ITC, Cargill, Dabur, HLL Amalgam Foods, Radhakrishna, DCM Shriram, Tata group are now sourcing mainly from within the country rather than imports. Says Jai Bhagwan Singla, president of Haryana Yuva Vyapar Sangathan: "We have been trading in foodgrains since 1963 but have never seen such huge margins in wheat. Initially, traders were wary of the government. But when nothing happened and foreign companies began making massive purchases, we also got into the act." Now, after the import liberalisation, futures prices are set downhill, affecting small traders and stockists.

ICRA economic advisor Saumitra Chaudhuri says that "it is a good thing our inflation threshold (of discomfort) now appears to be 5 per cent compared to 8 per cent even a few years ago". It could go down more, but the fact remains that inflation may climb further and end the year at 6 per cent. As a result, further tightening by the rbi is expected. With increasing commercialisation of agriculture and farmers shifting from food crops to more lucrative commercial crops, the good old days of cheap food are certainly over.