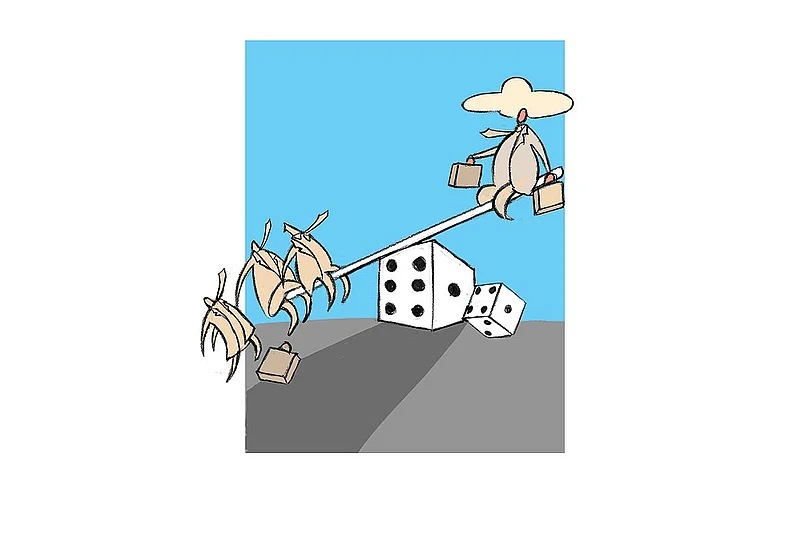

In a recent interview, the legendary Vinod Khosla estimated that 85 per cent of Indian start-ups are overvalued and will come to grief. He was being optimistic, and he knows it. As a long-term venture capitalist, Khosla is inured to operating in an industry where the strike rate is roughly 1:10. What that means is: one in ten businesses ends up recouping the investment poured into it. A trivial mental calculation shows that one successful business must generate returns of over 10:1 for the VC industry to survive. This high-risk-to-high-return ratio is hit often enough for VC (and its sibling, the private equity, or PE, industry) to stay in business. PE has a better strike rate than VC because PE targets companies further down the road to profitability. Even so, the PE strike rate is also low.

Of course, the companies that do survive often do spectacularly well. For example, Apple, Microsoft, Dell and Hewlett-Packard were all tiny businesses started by college-going kids. Each hit a sweet spot in the economy and grew into a massive multinational, employing hundreds of thousands of skilled workers, generating employment for millions more, and making millionaires out of many of their shareholders.

Hundreds of kids in America, maybe thousands, must have started businesses in basements and college dorms, inspired by those success stories. Most of those businesses would have gone belly up, while a few were moderately successful. But we only hear about the improbably successful ones.

This is one big problem when it comes to making sense of the entrepreneurship bubble. All the attention is focused on the big successes, and occasionally, on the terrible disasters. The news is all about outliers. If you track entrepreneurship through the media, or even via academia, you will get no sense of the middle ground.

This is a classic example of what behavioural scientists call selection bias. Wikipedia definition: Selection bias is the selection of individuals, groups or data for analysis in such a way that proper randomisation is not achieved, thereby ensuring that the sample obtained is not representative of the population intended to be analysed.

What happens to the vast majority of people who start high-risk businesses, or take risks to try and expand small existing businesses? Most high-risk new businesses are unsuccessful. And most risks do not pay off.

Even serious academics can display selection bias. The Millionaire Next Door, for example, was a book that recast a series of academic case studies and became a pop bestseller, which it well deserved to be. The author, Thomas Stanley, started studying the affluent in the 1970s, at the request of the New York Stock Exchange. Over decades, Stanley met and studied thousands of “unassuming” millionaires. His subjects were people who had built fortunes by unglamorous means. He spent a lifetime deciphering commonalities in lifestyles, work habits and investing patterns. It’s an interesting book (as are the follow-ups). But anybody reading it might make the mistake of assuming that somebody, anybody, who had certain habits and a given lifestyle would automatically become a millionaire.

That’s simply not true. About three per cent of the US population have assets of $1 million or more. Leaving aside the Silicon Valley and biotech successes, and the high-flying lawyers and doctors, many of the millionaires fall into the Stanley stereotype of running unglamorous businesses, living frugal lifestyles etc. But there are many others who work just as hard, are just as smart and simply not as successful. Luck, timing, who-knows-what, plays a part in achieving success.

A look at India’s own business communities will suggest this is equally true here. Most of India’s iconic businessmen were famously frugal; they often deliberately ran unglamorous businesses (partly due to a common fear of the taxman); they made smart investment decisions. But for every G.D. Birla, there are thousands of small businessmen who never cracked the big time.

It’s great that India’s entrepreneurship ecosystem has now developed to the point where dreamers can be actively encouraged to dream big and they can tap into funding and mentoring to help shape their dreams into reality. Every success story will create employment, generate wealth and encourage yet more youngsters to dream. But there is a cold unpalatable truth which we should remember when celebrating those successes: there will be many failures for every success story.

This brings us to one very critical difference between India’s socio-cultural environment and that of America. America rewards successful entrepreneurs. But more than that, America forgives the failures. It is perfectly alright for an individual in America to launch a start-up which goes bankrupt, and to pick up the pieces and launch yet another start-up. There is no shame or social opprobrium attached to such business failure.

Indian society—our samaj and sansrkiti—must learn that trick. For it is central to enabling entrepreneurship. If you want to encourage entrepreneurship, you must learn to forgive failure.