July 29, 2021, was the 67th birth anniversary of ‘Big Bull’ Harshad Mehta, an ambitious and optimistic investor-speculator who played a crucial role in inculcating and deepening the investment cult in the Indian capital market. On that day, social media was flush with backhanded eulogies on the master manipulator. “Happy Birthday legend…Thank you for creating interests of many haters towards stock market…They will hate you but can’t ignore you.”

During his short life of 47 years—he died on December 31, 2001—Mehta used unethical, and sometime illegal, means to play the markets. In a Bollywood movie inspired by Mehta, the protagonist is warned by the head of the stock exchange: “What you do is insider trading. There is no law against it in India. In the US, you would be in the prison for decades.” Mehta’s character retorts: “Bring in the law, and then I will think about it.”

Advertisement

But despite the fact that he was arrested and died an untimely death, the Big Bull of the 1990s wooed thousands of small investors to the stock market. In 1991-92, when his buying was at its peak, people saw him as the new Midas, as every stock he touched or whispered about, boomed and zoomed. Even after he was exposed as a villain in 1992, and the stock market crashed, investors were crazed about stocks. This was evident during the subsequent IPO frenzy (1993-97).

Stock exchages went online

Advertisement

This marks a huge difference between how the masses reacted to stock scandals and cycles of booms and busts in the decades before 1991, when reforms kicked in, and the years that followed. Until the eighties, the scams unnerved, scared and scarred investors, who ran and stayed away from the capital markets. In the past 30 years, frauds and disruptions due to external shocks goaded them to return in greater numbers, and with higher amounts of their savings.

ALSO READ: When Liberalisation Freed India Inc

Overall, this is what has transformed the financial markets. Four decades ago, in 1981, the combined value of the listed companies, which were part of the 30 largest business houses and accounted for the bulk of the market capitalisation, was Rs 6,200 crore. At that time, India’s GDP was 28 times larger, or Rs 1.75 lakh crore. Today, the market cap of the listed firms on the National Stock Exchange (NSE) is almost 15 per cent more than the country’s GDP of Rs 197 lakh crore.

Yet another way to gauge this change is through incremental jumps of 5,000 points each in the Sensex, the Bombay Stock Exchange (BSE) index, on its journey to 50,000. The Economic Survey (2019-20) states, “Sensex has not only grown after 1991, but has grown at an accelerating pace. Whereas crossing the first incremental 5,000 points took over 13 years from its inception in 1986, the time taken to achieve each incremental milestone has substantially reduced over the years.”

What is relevant is that the higher the index was, the faster it added the next 5,000 points. “Note that the acceleration in the Sensex was not due to the base effect. In fact, the higher acceleration stemmed from higher cumulative annual growth rate (CAGR),” adds the Survey. The index touched 5,000 in October 1999; it was at 4,000 during the heights of Mehta’s machinations in 1992. The 10,000 mark came in February 2005, and 20,000 in less than three years (December 2007).

Advertisement

Of course, the Financial Crisis of 2008 slowed down the pace, and the next milestone of 25,000 took six-and-a-half years i.e., by June 2014. The 30,000-mark was crossed in less than three years, by April 2017, and 35,000 within a few months, i.e., January 2018. In another 17 months, the Sensex crossed 40,000 (June 2019), and despite the crippling Covid crisis, it is almost 55,000 in just over two years. During this 46-year-long journey, there were several setbacks, crises and scandals.

Let’s compare what happened during the ongoing Covid pandemic, which initially ravaged the stock indices, with the instability and precariousness of the markets during the 1950s and 1980s. In March 2020, Sensex crashed by 40 per cent. By November the same year, it was back to its earlier peak. The rise and rise of the Sensex continued. Now, it is more than double the lowest point last year and almost a third higher than its level in January 2020.

Advertisement

The number of investors’ accounts on the BSE jumped three-fourths to 70 million between end-March 2020 and early-July 2021. Almost 15 million new demat accounts were opened at the BSE and NSE depositories during the same period. Despite the ups and downs in stock prices in the past 16 months, and economic uncertainties, more people now own shares, and trade on the two exchanges. A Calcutta-based day-trader says, “Most of my friends have joined the bandwagon.”

V.K. Vijayakumar, chief investment strategist at Geojit Financial Services, explains, “Retail investors account for 45 per cent of cash transactions, a big jump from 33 per cent five years ago. During the same period, the share of foreign portfolio investors (FPIs) fell sharply from 23 per cent to 11 per cent. The domination of retail investors explains why markets do not correct when FPIs sell continuously. But most retail investors are driven by sentiments and momentum, not fundamentals.”

Advertisement

Investors are younger; the new ones largely comprise millennials in the 18-36 age bracket. “Our customer on-boarding surged in 2020-21, and we added two million new customers and doubled the base. Of the new additions, 80 per cent are between 18 and 36 years, and 70 per cent are first-time investors,” says Ravi Kumar, co-founder and CEO of Upstox, a discount brokerage that is backed by Ratan Tata and Tiger Global. Many invested in mutual funds, whose assets soared.

At the same time, a substantial percentage of the new investors hail from Tier-2 and Tier-3 cities. Kumar says that 80 per cent of Upstox’s customers are from such places. “The maximum number of first-time investors belongs to Tier-2 cities such as Jaipur, Aurangabad and Warangal. Among the Tier-3 locations, Karimnagar, Rangareddy and Ahmednagar lead,” he adds. Of the 70 million existing investor accounts with the BSE, the state-wise composition includes: Maharashtra over 21 per cent, Gujarat over 12 per cent, Uttar Pradesh almost 7.5 per cent, and Tamil Nadu and Karnataka with 6 per cent each.

Advertisement

Cut to 1957, when independent India witnessed one of its first prominent stock scams, which resulted in skyrocketing prices, followed by a deafening crash. Between March and September that year, the state-owned LIC purchased shares in several concerns owned by Haridas Mundhra. For example, on June 24 and 25, LIC spent Rs 12.69 million in off-the-market deals to shore up the prices of Mundhra’s stocks, and to stabilise the stock markets. The strategy failed dismally.

Between June 24, 1957 and January 16, 1958, the stock indices tumbled. The shares of Mundhra-owned companies went into a free fall, and the declines were much higher than the others. For example, blue chips like Tata Iron & Steel, Indian Iron & Steel and ACC were down by 1.5, 2.9 and 5.1, respectively, during the period. As against these, the depreciation in the values of the Mundhra-controlled British India, Osler Electric and Richardson & Cruddas ranged between 30 per cent and 50 per cent.

Advertisement

The Chagla Commission, which investigated the scandal, pinpointed Mundhra as a manipulator with Harshad Mehta-like traits. Mundhra had a “flamboyant personality”, was a “financial adventurer”, and “suspected to be a law-breaker”. He possessed a “doubtful financial reputation”, and his “antecedents were of a most questionable character”. His ambition was to “build an industrial empire by dubious methods”, and he employed any means “so long as the end is achieved”.

Worse, various investigations, including exposes by Feroze Gandhi—Indira Gandhi’s husband and Prime Minister Nehru’s son-in-law—found that the decision to ask LIC to purchase the shares was initiated by then finance secretary H.M. Patel. His boss, finance minister Tiruvellore Thattai Krishnamachari (TTK), was aware of it. RBI governor H.V.R. Iyengar and SBI chairman P.C. Bhattacharyya knew about it. LIC’s top officials, including its chairman C.R. Kamat and managing director L.S. Vaidyanathan, followed “orders” from the top.

Advertisement

Although the scandal had political ramifications—TTK resigned and Nehru was under considerable pressure—it had minimal impact on the stock market. Retail investors continued to shy away from stocks, as they believed that the exchanges were dens for speculators, gamblers, and thieves. The markets were, therefore, thin, and unregulated. There were multiple exchanges, including the ones in smaller cities like Ludhiana, and they generally thrived on manipulations by the insiders.

The situation remained the same until the beginning of the eighties. Two personalities, a corporate tiger and yet another big bull, wooed back the mass investors. After going public in 1977, Reliance Industries, which was promoted by the late Dhirubhai Ambani, came up with innovative instruments to enthuse its shareholders. The late M.J. Pherwani, who headed the Unit Trust of India, which had huge cash, went on a relentless buying spree. The combo spurred the stock markets.

Advertisement

ALSO READ: The Healthy Paranoia

Shopkeepers, taxi drivers, home-makers and household helps, office-goers, and factory workers queued up to buy Reliance shares. At the annual shareholders’ meetings, many claimed that they managed their daughters’ weddings and illegal dowries, paid for their children’s education, and went on vacations because of the profits they made from the sale of the Reliance shares. When state-owned fertiliser firms went public, they roped in farmers to buy their stocks.

Obviously, the boom led to illegalities. Promoters sold their shares in illicit markets at high prices. Prices of the shares in the grey markets were hiked up, even as cartels propped up certain stocks in the regular markets. No one was sure, which stocks were rigged and which were genuine. Fly-by-night operators issued stocks which, years later, led to vanishing promoters and companies. As the boom petered out, it left scores of investors licking their wounds and holding worthless paper.

Advertisement

For the next few years, investors shunned the markets, i.e., until Mehta lured them back in 1991. From then on, it was a non-stop series of wild parties, followed by bad hangovers. Investors made pots of money when prices went up; they lost everything during the slumps. Yet, they came back to join the next revelry, aided by the growing number of newcomers, who wanted to partake in the new paper wealth. Each generation—X, Y, Z, and millennials—was excited.

One can think of several reasons why this happened, and why investors stayed invested despite the regular shocks and scams. The first is that the policymakers made genuine, though half-baked, attempts to make the markets safe and secure. There were policies to protect the small investors, and a regulator, albeit toothless, was in place. New options like mutual funds were available. Most of these decisions were triggered by the governments’ zeal to attract foreign investors.

Advertisement

Disclosures underwent a sea change, and resulted in quality information for the shareholders. This increased investors’ confidence, particularly among the new and younger buyers. Jimeet Modi, founder and CEO of Samco Group, explains, “The next few decades in the capital markets will be driven by transparency, equality and safety. A bunch of reforms were undertaken on these fronts in the past few years. However, we will need to make further progress in the years to come.” Second, making money and wealth accumulation were no longer considered a social stigma. Successive generations, whose incomes went up in comparison to their predecessors, had more disposable earnings to save and invest to fulfill personal future desires, and those of their children. Money begets money was a mantra that we learned. And it was considered a disgrace to keep the money idle in savings accounts and fixed deposits.

Advertisement

The digital flourish boosted digital-based trading and investing, and tech-savvy millennials with higher risk appetites than the previous generations adopted it. New technologies narrowed the gap between institutional and retail investors. The small investor now had the same tools, data analytics and access to information as the bigger players. The proliferation of smartphones and low-cost data were other boosters. This led to large-scale democratisation of the markets.

In the immediate future, higher retail participation in equities can have two major impacts. It will increase the share of savings through shares and debentures as a percentage of total household financial savings. From a figure of 3.4 per cent in 2019-20, it can easily climb up to 5 per cent. Nations like the US (36.5 per cent) and China (11 per cent) are ahead, and indicate the upside that India can witness. Digitisation can, and will, surely hasten this ongoing process.

Advertisement

ALSO READ: Beyond Shibboleths

Higher savings, in whatever form they come, and equity savings can allow larger resources to be available to finance large infrastructure projects, feels Soumya Kanti Ghosh, chief advisor of the State Bank of India Group. This will help the country to become a $5 trillion economy faster. Most importantly, the wealth of the small investors will surge. As Jimeet Modi puts it, “We believe that retail investors will capture the highest share of wealth, as compared to the other sections.”

***

Brand Equity: Wealth Index

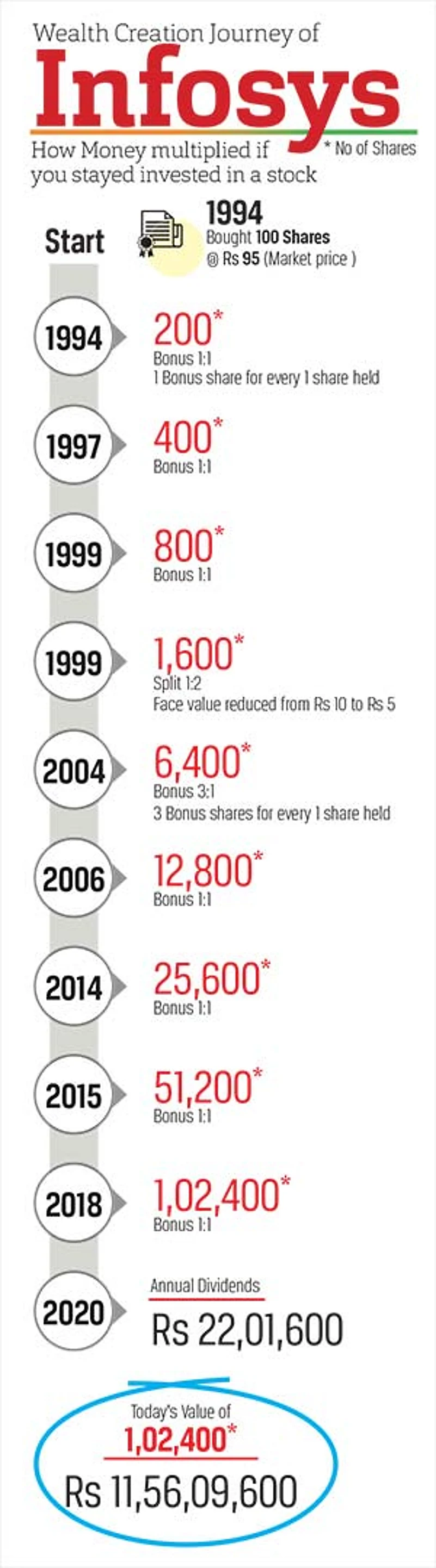

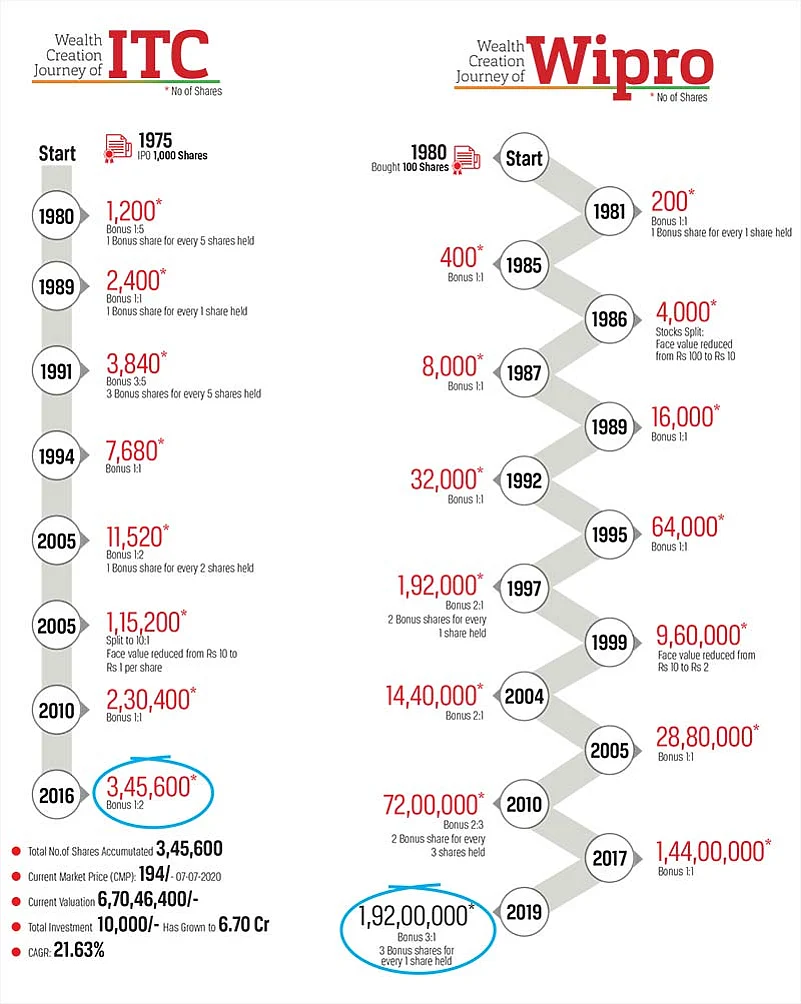

Historically, it is proved that equity investors created more wealth from their initial investments. Stocks which generated stupendous profits for the buyers include Wipro, Eicher Motors, ITC and Infosys. According to Vinit Bolinjkar, head of research at Ventura Securities, equities play a big role in financial inclusion, as such investments help people to put money in businesses that suit their preference for risks and returns. It helps borrowers to meet enterprise needs and risk appetite.

Advertisement

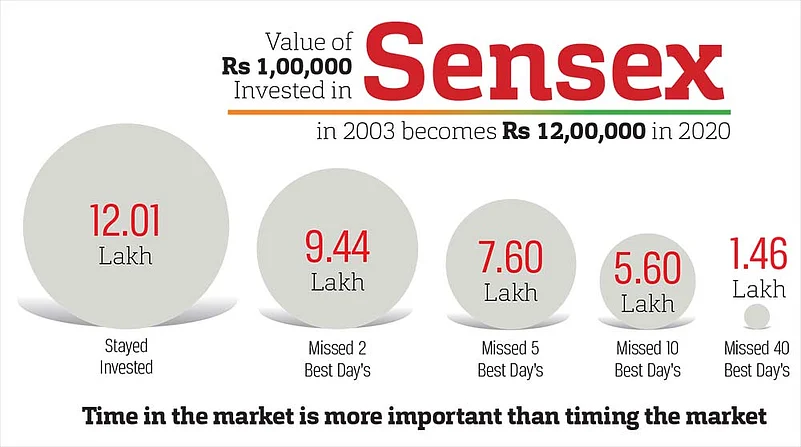

However, he warns that this form of wealth creation happens in the long run. “Equity is a tool for the long term, rather than short-term gambling,” adds Bolinjkar. Stocks are typically associated with volatility in the short run, and there are risks. Over time, financial discipline can help individuals. It is important to remain invested, and not try to time the market. Shares are among the most liquid assets (provided you invest in the right stocks), and the capital requirement is low.

***

Digital Bharat: The Way Ahead

Digitisation helped policymakers to bring the unbanked rural poor into the formal banking sector. Various state governments and large banks undertook projects through self-help groups (SHGs) to achieve this objective. Uttar Pradesh (UP), which has 75 districts and is the largest state, is an example. In the state, the quantum of informal transactions that happens in rural areas, mostly in cash, amounts to more than Rs 1 lakh crore annually. To formalise it, the state government partnered with the banks to on-board business correspondents (BCs) in each of the 58,000 gram panchayats.

Advertisement

This was done through Uttar Pradesh State Rural Livelihood Mission. Within the local SHG, a woman, BC Sakhi, was appointed to provide banking services at locations other than bank branches and ATMs. After the on-boarding, PayNearby works to up-skill BC Sakhis on the use of the digital ecosystem, and digital solutions to enhance financial inclusion. Anand Kumar Bajaj, founder, MD and CEO of PayNearby, explains, “While the BC model ensures low-cost delivery of accessible banking services to every section, the SHG platform has proven to be pivotal in this task, owing to its comprehensive reach and influence.”

Digitisation also helps farmers through commodity derivatives trading. Increased participation has not only facilitated efficient price discovery in the futures market, but contributed to financial inclusion. It has empowered farmers with increased bargaining strength, as the price information is freely and transparently disseminated through various electronic platforms. Small and marginal farmers can also participate in the futures trading and hedge their produce. Naveen Mathur, director (commodities and currencies) of Anand Rathi Shares and Stock Brokers, says, “With the launch of new products, the derivatives market will look more vibrant. The permission to allow mutual funds to participate in derivatives will not only deepen but broaden the markets.”

Advertisement

(This appeared in the print edition as "Here’s the Money, Honey!")